INTERMEDIARY ONLY

Simpler bridging for every project

Online calculators and applications gets you instant quotes and Heads of Terms in minutes

Financing up to

£30 million

Interest rates from

0.82%

Max LTV

85%

Term length up to

18 months

Product guide

All about our bridging products

Key features

Highlights

Rates from 0.82% per month

Refurbishment Bridge via the portal up to 73% net LTV

Regulated and Unregulated

Residential, semi-commercial, commercial and land

Terms up to 18 months

Flexible minimum interest periods

1st charge (Unregulated and Regulated) or 2nd charge (Regulated Bridge only)

Serviced, retained and rolled interest

Title insurance

Free legals and valuations to refinance your loan to BTL (standard properties only)

Refurbishment GDV up to 70% LTGDV and max 3 drawdowns not via the portal

Refurbishment Bridge via the portal up to 73% net LTV

Regulated and Unregulated

Residential, semi-commercial, commercial and land

Terms up to 18 months

Flexible minimum interest periods

1st charge (Unregulated and Regulated) or 2nd charge (Regulated Bridge only)

Serviced, retained and rolled interest

Title insurance

Free legals and valuations to refinance your loan to BTL (standard properties only)

Refurbishment GDV up to 70% LTGDV and max 3 drawdowns not via the portal

Pricing

For all our bridging rates and more information, please view our product guide

Application process

Overview

For all your bridging cases, please login to the portal to apply.

If you wish to discuss your deal before applying, please contact: 0203 836 1837.

For the Refurbishment GDV product please contact the team as this is not available in the portal: [email protected].

If you wish to discuss your deal before applying, please contact: 0203 836 1837.

For the Refurbishment GDV product please contact the team as this is not available in the portal: [email protected].

More information

More information about Bridging can be found in our criteria guide.

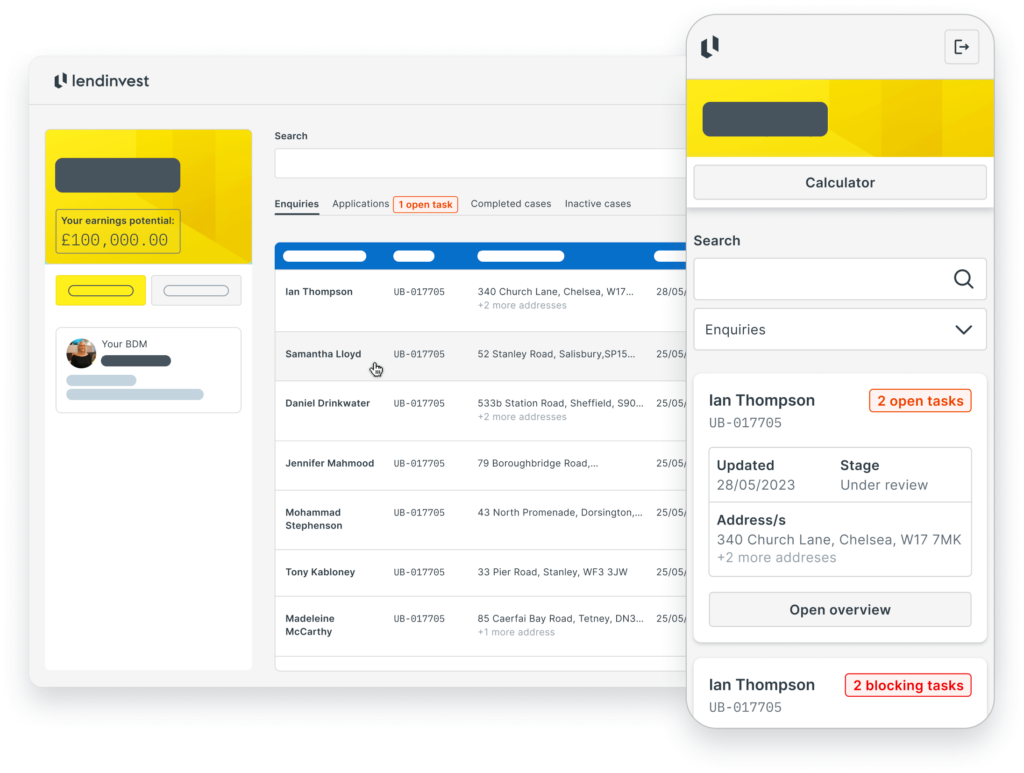

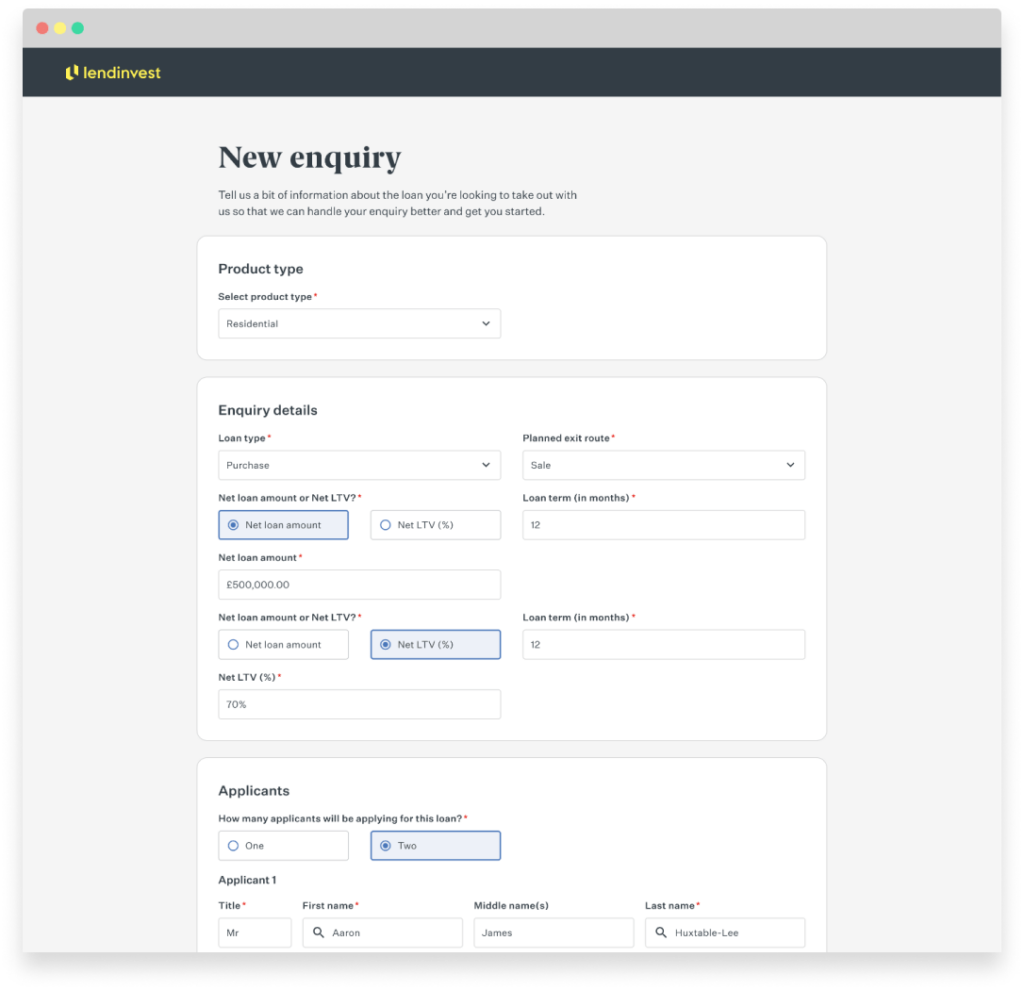

Submitting an enquiry in minutes

When you’re registered for the portal you can submit the easiest bridging enquiry on the market:

1. Click new enquiry

2. Choose between our Regulated Bridge, Auction, Bridge-to-Let, Development Exit, Residential Bridging, Commercial Bridging and Refurbishment products

3. Fill out basic enquiry details

4. Find your security property in our address finder and share the value

5. Tell us about your deal

6. Upload your documents

7. Submit your enquiry

2. Choose between our Regulated Bridge, Auction, Bridge-to-Let, Development Exit, Residential Bridging, Commercial Bridging and Refurbishment products

3. Fill out basic enquiry details

4. Find your security property in our address finder and share the value

5. Tell us about your deal

6. Upload your documents

7. Submit your enquiry

Simple applications built around you

From start to finish, every one of your bridging deals can be managed within the portal. For Unregulated Bridging, you get added benefit of:

E-signatures for your clients helps speed up the process

Transition from enquiry to completed application in minutes

10 clicks from start to Heads of Terms

“LendInvest is a no-fuss specialist lender with great people to deal with and they lend in all scenarios.”

John Demetriou, jmdmortgages LTD

CASE STUDIES

Experience that speaks for itself

Take a closer look at the types of deals you can deliver your clients

Leeds

Loan amount

£5,200,000

LTV

63%

Terms

12 months

Cambridge

Loan amount

£3,200,000

LTV

63%

Terms

12 months

High Wycombe

Loan amount

£1,050,000

LTV

70%

Terms

12 months

Useful tools

Download guides and reference documents