Navigating the Property Market in the UK: A Comprehensive Look at 2023 and Strategic Insights for 2024

With a backdrop of high inflation and escalating interest rates throughout 2023, investors are likely to encounter a pivotal moment in 2024. In this article, we will explore the changing market conditions in 2023, offering insights into some of the potential advantages of real estate debt as a possible investment strategy for eligible professional investors looking to navigate the twists and turns that may lie ahead.

2023: A year of contradictions

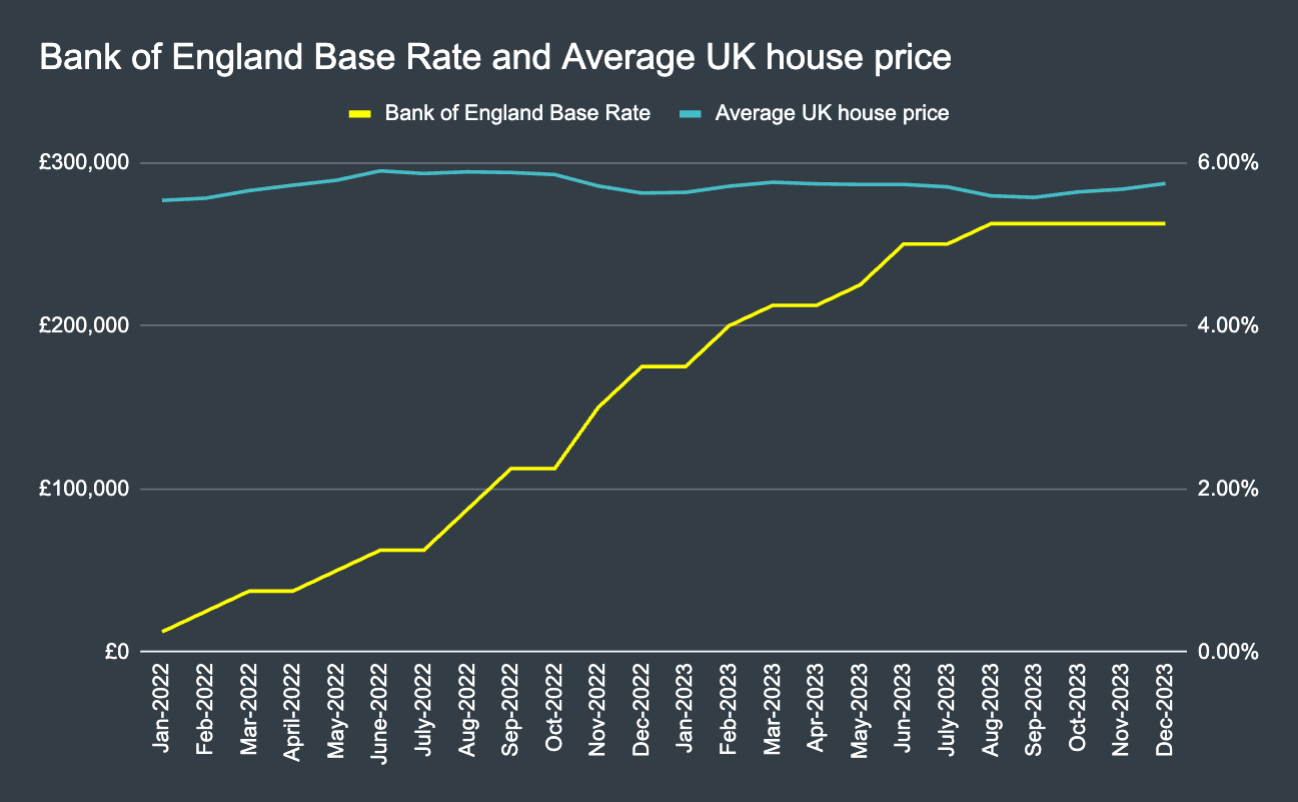

In 2023, the Bank of England base rate surged to its highest level since the 2008 financial crisis, peaking at 5.25% in August and remaining at that level since (Source: Bank of England). Yet, the housing market’s resilience exceeded all forecasts provided by market commentators, including our in-house view which predicted an annual drop of 5%-7%. According to Halifax, house prices not only didn’t drop, they grew by 1.7% (although Nationwide reported a slight dip of 1.8%), challenging the belief that higher interest rates necessarily slow the housing market.

Figure 1: Bank of England Base Rate vs Average UK House Price (ONS)

The market’s stability amid climbing interest rates was supported by factors such as a noticeable drop in construction starts since the onset of COVID-19, contributing further to the chronic housing supply scarcity. Furthermore, the downward pressure on pricing caused by higher interest rates was partially offset by robust rental growth, evidenced by a 5.7% increase in private rental levels, highlighting resilient demand (ONS).

In addition, after peaking at 11.1% in October 2022, inflation dropped throughout 2023 reaching 4% in the 12 months to December. As a result, wage growth outpaced inflation (ONS), further alleviating cost-of-living pressures and enhancing affordability for potential homebuyers.

Examination of the housebuilding industry reveals the profound impact of the challenges faced in the past year. Marked by the cessation of Help to Buy, escalating build costs (although pressure has eased since), and a shift in planning policy, smaller housebuilders and first-time buyers bore the brunt of these developments. Combined together, these effects translated into a squeeze on developer profits, a small decline in development land values, and an observable impact on the industry’s capacity to deliver new homes at scale.

2024 Projections

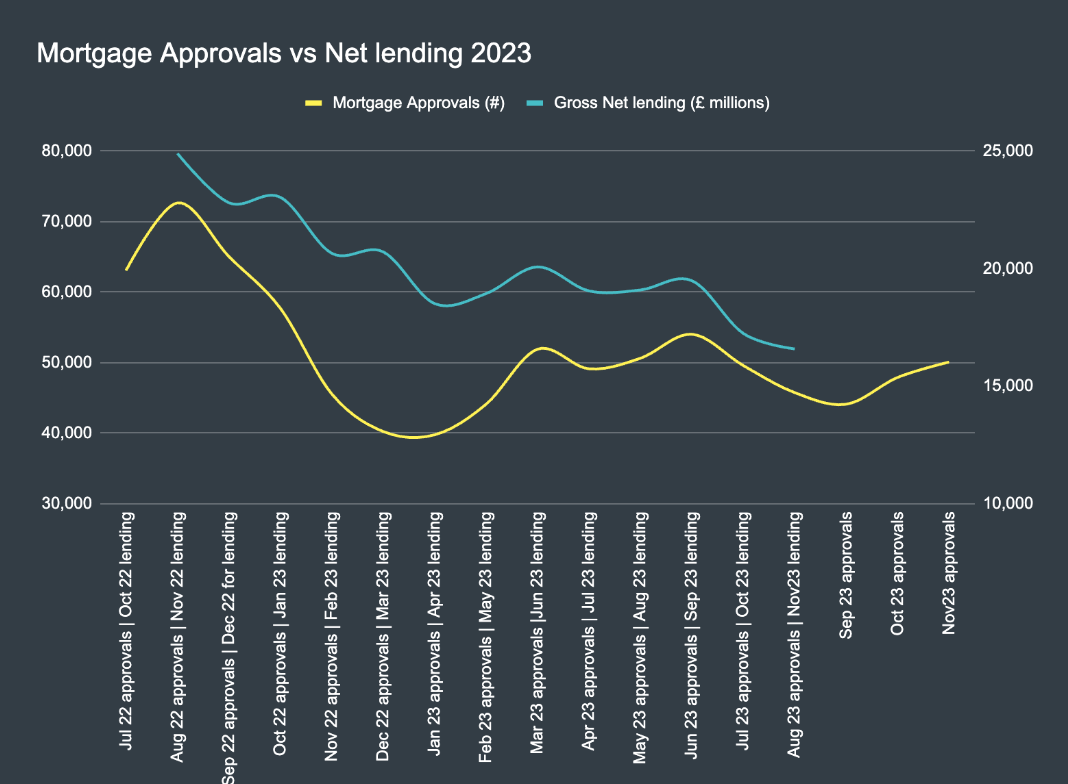

As we step into 2024, early indicators suggest the activity in the market will start to pick up in the first quarter, with mortgage approvals rising at the end of last year (see figure 2).

Figure 2. Mortgage approvals vs Net lending 2023. Source: Trading Economics.

*The lending data in the figure above is offset by three months to demonstrate the typical lag from when a mortgage is approved and when the process completes.

Notwithstanding this positive leading indicator, challenges persist with inflation still above the Bank of England long-term target of 2%, and Governor Andrew Bailey indicating that the Base Rate will be held at 5.25% for the foreseeable future. Following a surprise increase in inflation in December 2023, market conditions are expected to improve gradually, translating into a steady recovery rather than a swift rebound. Affordability enhancements are forecasted, driven by expected income growth, moderately lower house prices, and decreasing mortgage rates. If the economy lingers and mortgage rates moderately decrease, our expectation is that house prices are likely to remain flat or witness a slight decline throughout the year.

While the cost of debt is projected to stay “higher for longer”, anticipation of progressive cuts in the cost of mortgage debt over the next five years suggest a potential resurgence in house price growth and heightened market activity in the short to medium term. The prospect of reduced mortgage costs is likely to benefit a diverse range of buyers, by alleviating pressure on budgets for both owner-occupiers and investors.

Despite uncertainties linked to a general election, the political landscape presents positive indicators for UK housing development. As the current government has failed to deliver its promise to deliver 1 million new homes during its tenure, Labour has taken the opportunity to position itself as a proponent of housing delivery and homeownership. A series of recent Labour policy announcements, including a pledge to deliver 1.5 million new homes over the next parliament, planning reforms, town development plans, and proposals for planning passports for urban brownfield land, signal a robust agenda. In response, the Conservatives have revisited their housing offer, acknowledging the need for reform.

Whilst the timing and outcome of a general election remain unknown, it looks increasingly likely that UK development will receive the boost that it needs to recover from the effects of 2023.

Real Estate Debt Strategies

As the UK housing market begins to recover and the demand for housing returns, we expect to see an increase in real estate investment activity in 2024. Despite the positive outlook, the uncertainty around house price growth means investors might look to explore debt-based investments over equity-based alternatives. Such investments have historically been able to provide steady, reasonably non-correlated returns. The growing demand for housing requires a rise in borrowing to facilitate property transactions, and we are already observing an upward trend in both finance applications and approvals compared to this period in 2023.

Moreover, in the event of an unforeseen market downturn, real estate debt—secured against real assets—can serve as a buffer against value depreciation, potentially providing a layer of security amid uncertainties.

Due to the less liquid nature of properties, investors are urged to focus on long-term trends to obtain the maximum benefit from the real estate market over the coming years.

The real estate market stands at the crossroads of challenges and opportunities as we transition from 2023 to 2024. Navigating these complexities requires a strategic approach. By understanding the nuances of high-interest rates, resilient house prices, and evolving economic indicators, investors can position themselves to harness the potential for positive returns while mitigating risks. As the market dynamics continue to unfold, adaptability, resilience, and a forward-thinking mindset will be key to navigating the ever-evolving real estate landscape.

—-

Any and all information about investing is only intended for eligible investors. Investors must meet the investor eligibility criteria, including, for our funds, that they are well informed and, where relevant, have sufficient investment knowledge, experience and financial resources. The LendInvest Secured Credit Fund II is not available to retail clients.

The LendInvest Self-Select Platform is a non-mass market investment and not suitable for all investors. Don’t invest unless you’re prepared to lose all the money you invest. This is a high-risk investment and you are unlikely to be protected if something goes wrong. Take 2 mins to learn more.

For Self-Select Platform queries, contact: [email protected].

Income and capital repayments are not guaranteed. Investors cannot liquidate investments, but the underlying borrowers may repay early, late or not at all. Your capital is at risk.

Past performance is not a reliable indicator of future results. The information we provide can help you make your own informed decisions, but it is not investment advice or a personal recommendation.

You should ensure you fully understand the risks. You should seek independent financial advice if you are not sure a product or investment is right for you, or you do not fully understand the risks.