Bank of England cuts Interest Rates by 25bps to 4.50% – A Positive Step, But the UK is Still Lagging Behind

Written by Hugo Davies

Written by Hugo Davies

The Bank of England has finally acted, cutting the base rate by 25 basis points to 4.5%.

This long-overdue move will begin to ease borrowing costs across the UK economy, including for homeowners, landlords, and property developers.

But the bank could have, and perhaps should have, gone further today – with two of the nine-person BoE panel advocating for a 50bps cut, which would have dropped the rate to 4.25%.

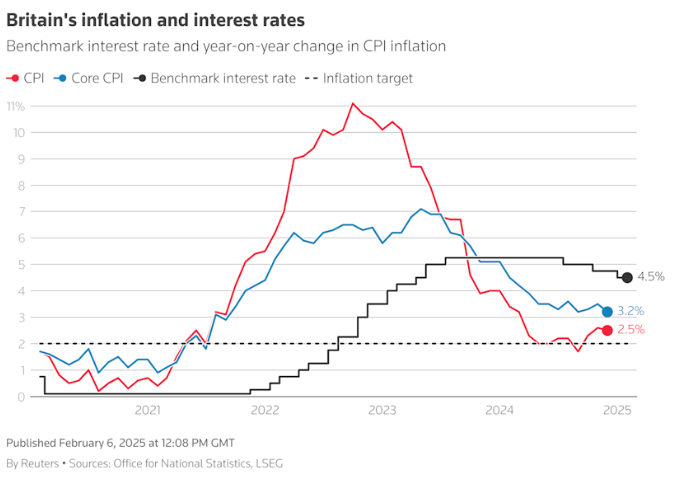

Courtesy: Reuters

High interest rates have stifled housing market activity, restricting access to mortgages, making property development more expensive, and limiting investment in rental and regeneration projects.

For borrowers, developers, and property investors, this is a step in the right direction – but it is not enough. The UK remains far behind other major economies, where central banks have already moved more decisively to support lending markets.

The European Central Bank has cut rates five times since mid-2024, bringing its deposit facility rate down to 2.75%. The US Federal Reserve is expected to deliver multiple rate cuts this year to ease economic pressures.

By comparison, today’s move by the BoE feels tentative, with a 7- 2 vote in favour of a cut, driven by near-term cautiousness around services inflation and the potential impact of new fiscal measures on hiring. It implicitly acknowledges that borrowing costs must come down to support the economy as it begins to stall, but falls short of delivering the meaningful rate relief needed to unlock housing market growth, boost confidence and stimulate activity.

What was perhaps more telling was that two of the panel – Catherine Mann and Swati Dhingra – voted to cut the rate by 50bps – a move LendInvest would certainly have welcomed.

Cut the Complex with LendInvest

Swap Rates: The Other Key Factor Shaping Borrowing Costs

While a base rate cut is an important step, it is not the only factor determining the cost of property finance. Swap rates also play a crucial role in shaping mortgage pricing and development finance costs.

Swap rates act as a stabiliser for lenders, allowing them to hedge against potential interest rate fluctuations and ensure more predictable returns when offering fixed-term loans. However, they are heavily influenced by broader market confidence. If the Bank of England does not provide clear guidance on its future rate trajectory, lenders and financial institutions struggle to anticipate the long-term cost of lending. This uncertainty fuels volatility in swap rates, ultimately pushing up borrowing costs.

This is exactly what we have seen over the past year. Two-year swap rates surged to 4.44% in early 2025, their highest level since July 2024, while five-year swaps climbed to 4.31%, the highest since November 2023. Market volatility and unclear signals from the Bank of England have made it difficult for lenders to price fixed-rate mortgages and development finance with confidence. The 2 year swap has since fallen by 0.44% and the 5 year swap by 0.46% since those highs just a matter of weeks ago.

While the Bank of England does not control swap rates outright – global economic trends, inflation expectations, and investor sentiment all play a role – it does have a responsibility to provide clarity. More consistent guidance on its interest rate plans would help stabilise swap markets, giving lenders the confidence to price borrowing more predictably, giving brokers greater conviction to deliver solutions for their customers who are often making some of the biggest financial decisions in their lives. Without this, financing across the housing market remains exposed to swings.

UK Property Market Holds Firm, Despite the High Cost of Borrowing

Despite the prolonged period of high interest rates, the UK housing and property investment market has remained resilient.

Nationwide’s latest House Price Index shows that house price growth slowed to 4.1% in January, down from 4.7% in December, but prices still edged up 0.1% month-on-month, bringing the average UK house price to £268,213.

While this shows that the market is still moving, the reality is that affordability is stretched.

A first-time buyer with a 20% deposit now spends 36% of their take-home pay on mortgage payments, far above the long-term average of 30%. While pressures remain, mortgage arrears have started to decline, with new figures out today from UK Finance showing homeowner arrears falling 2% in Q4 2024 and buy-to-let arrears dropping 3% – a sign that some affordability pressures may be easing.

However, while overall levels are still low by historical standards, possession numbers have increased, suggesting that for some borrowers, higher rates remain unsustainable.This does reflect the variety of support packages mortgage lenders have been providing, but it is not unreasonable to question this trend in the context of higher rates and a weakening jobs market.

Meanwhile, Dutch mortgage rates have already fallen below 4% as the ECB’s rate cuts filter through, reducing monthly repayments for homeowners. Irish borrowers have also seen mortgage payments drop by hundreds of euros per month after 1.35 percentage points of ECB reductions in 2024.

In contrast, UK developers and investors continue to face the highest property finance costs in Europe, restricting new projects and rental market expansion. Uncertainty around interest rate policy and volatile swap rates are prolonging affordability challenges, delaying the market recovery that borrowers and investors urgently need.