What Does the US Federal Reserve Rate Cut Mean for UK Property Investors and Borrowers?

Written by Hugo Davies

Written by Hugo Davies

LendInvest’s Chief Capital Officer and Managing Director for Mortgages weighs in on the US Federal Reserve’s rate cut and the impact it could have here in the UK.

After months of wrangling, dissent, and the occasional bout of social media pressure from the White House, the US Federal Reserve has finally cut interest rates. It lowered its benchmark rate by 25 basis points to a target range of 4%–4.25%.

It’s a move that follows persistent signs of a weakening labour market, with the Fed choosing to act pre-emptively to avoid a deeper economic slowdown, despite inflation remaining above target. The decision also came against the backdrop of increasing public pressure from the executive branch, raising uncomfortable questions about the independence of US monetary policy.

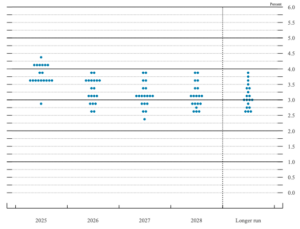

But with rates now cut and the Fed’s ‘dot plot’ (see below) pointing to two further reductions before year-end, the question for the UK market is: what does all this mean for property investors and borrowers here?

Let’s explore the implications.

For Borrowers: A Turning Point on the Horizon?

While UK inflation remains more stubborn than in the US or Eurozone, the Fed’s pivot is significant. It sets a tone for the global rate environment and sends a signal that the peak in rates is now behind us.

The Bank of England’s Monetary Policy Committee (MPC) crushed hopes of a further interest rate cut, keeping the base rate at 4%. This decision, with seven members voting to maintain the rate, reflects its ongoing concern about persistent inflation. The UK headline CPI inflation held steady at 3.8% in August, fuelled by rising food and drink costs. This cautious approach contrasts sharply with the Fed’s clear forward guidance and recent rate cut.

The Fed’s decision did not prompt an immediate response from the Bank of England. This underscores the MPC’s independent and cautious stance, but the decision does influence market expectations, helping to stabilise swap rates – a key driver of mortgage pricing for landlords and developers alike. Lower swap volatility brings more predictability to lending costs, and for many borrowers, that is half the battle. It also creates space for lenders to price more competitively, particularly on products funded via capital markets.

In short: while borrowing costs may remain elevated in the near term, the environment is shifting. And clarity breeds confidence, something sorely needed for development and refurbishment decisions.

Want more industry-led insights?

For Investors: Global Liquidity Starts to Loosen

For property investors and institutions allocating capital to credit markets, the Fed’s move offers a different kind of signal.

Lower US rates, and the promise of further cuts, drive investor demand for higher-yielding, risk-adjusted assets. In other words, as interest rates fall, institutions (like banks and pension funds) seek investment opportunities with higher rates of return. That brings greater appetite for private credit, mortgage-backed securities, and other real estate debt instruments.

As global borrowing costs begin to ease, particularly in response to moves by major central banks like the Fed, we may start to see previously stalled property projects come back to life. Lower rates can improve viability for developers, reduce the cost of refinancing, and make new investments more attractive, especially where projects were paused due to high debt servicing costs.

The UK, still offering relatively strong risk-adjusted returns, may become increasingly attractive to global capital, particularly as swap rates stabilise and spreads normalise.

The Bigger Picture: The Dot Plot and Directional Clarity

The Fed’s quarterly “dot plot” is a crucial tool for understanding their collective thinking. As shown in the above graphic, this anonymous chart displays where each of the 19 Federal Open Market Committee (FOMC) members expects the federal funds rate to be in the coming years. While not a binding promise, the clusters of dots provide clear directional guidance. It is this transparency that gives the market a powerful signal to plan ahead. This contrasts sharply with the Bank of England’s more cautious approach, which offers little in the way of explicit forward guidance. For UK borrowers and investors, this lack of clarity can create a more challenging environment for long-term planning, making the Fed’s pivot and its clear communication all the more significant.

The Fed’s decision does not change UK monetary policy overnight, but it does shift the global direction of travel. And for both borrowers and investors, that direction matters. As the Bank of England looks ahead to its own rate path, balancing high services inflation with weakening economic output, the international context cannot be ignored. The world’s largest economy is cutting rates, which may encourage others to follow.

In the meantime, for UK property investors, this moment may well mark the beginning of a more stable, more investable environment. One where volatility softens and where the path ahead becomes just a little clearer.