What interest rate rises could mean for the UK housing market

by Rob Pritchard, Head of Funds Management

With residential at the heart of the strategy for the Real Estate Opportunity Fund, the state of the UK housing market is naturally at the forefront of all our underwriting and portfolio management decisions.

Whilst there are a number of factors influencing the market, interest rates are one of the most important, and given the recent change in direction of the Bank of England and central banks across the world, we wanted to share with investors our view on how this could influence the fund and steps we are taking to maximise its performance.

Low Rates, High Prices

At the beginning of the pandemic, many in the industry expected social restrictions and economic uncertainty to put off buyers. A resultant drop in demand and corresponding fall in house prices appeared to many, inevitable, and to an extent this did play out. Housing completions in April and May 2020 were 57% and 53% down respectively on the previous year, whilst the impact on prices during this period is less clear due to the low number of sales. Land Registry data was not available in April 2020 due to a lack of available transactions, but indicated a decline of 1.7% in May – the steepest decline since 2009.

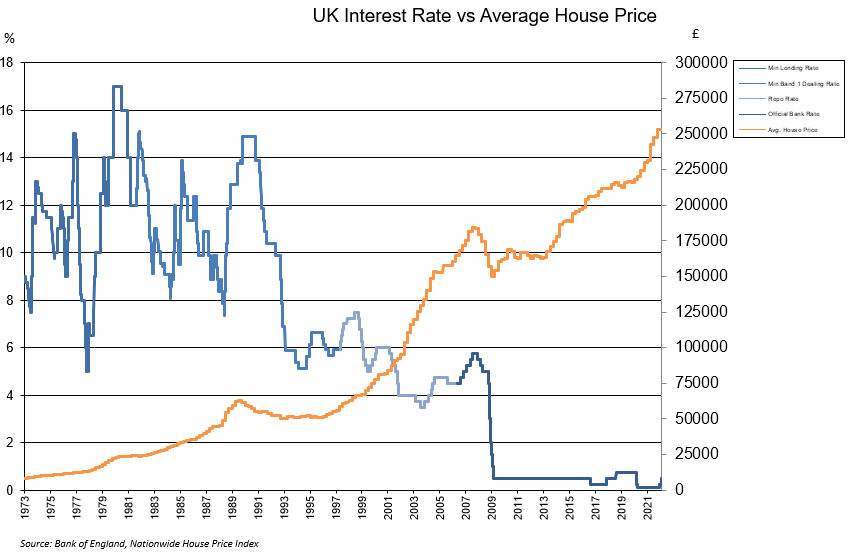

Yet, since those initial months of the pandemic, the UK residential market has performed exceptionally well. The total value of all UK homes reached £8.4 trillion in 2021, a new record high, with annual house price growth of 11.2% in January 2022, and many of our international investors will be well aware that this phenomenon is not just limited to the UK. The past 18 months has seen house prices surge across the majority of developed markets, underlining the demand for housing globally.

Since the global financial crisis, one of the few constants in the UK, through the Covid-19 pandemic and other major domestic events (anyone remember Brexit?), has been the policy of the Bank of England (“BoE”) to maintain record low interest rates. This has coincided with a period of significant house price growth, with UK house prices increasing 64% since the BoE dropped rates to their then record low of 0.5% in March 2009.

A Changing Environment

As the world emerges from the pandemic and inflation surges, the interest rate environment appears to be moving in a different direction to the one in which we have become conditioned to accept as normal. The BoE’s decision in February 2022 to raise the base rate (“BBR”) to 0.5%, represented its first back-to-back increase since June 2004. It is anticipated that this is the start of a series of gradual rate rises, with markets currently forecasting rates closer to 2% by mid 2023 before falling back to around 1%.

Whilst yield premium is the primary consideration for investors, homeowners are the real drivers of the UK housing market. For them, affordability is key and with 76% of home purchases made with a mortgage, the cost of that borrowing is critical to affordability. The theory is therefore that increased interest rates leads to higher mortgage rates, which in turn leads to reduced affordability and lower house prices.

It is difficult to deny the link between affordability and house prices, however, the question should be by how much do interest rate movements impact affordability and what other factors should be considered?

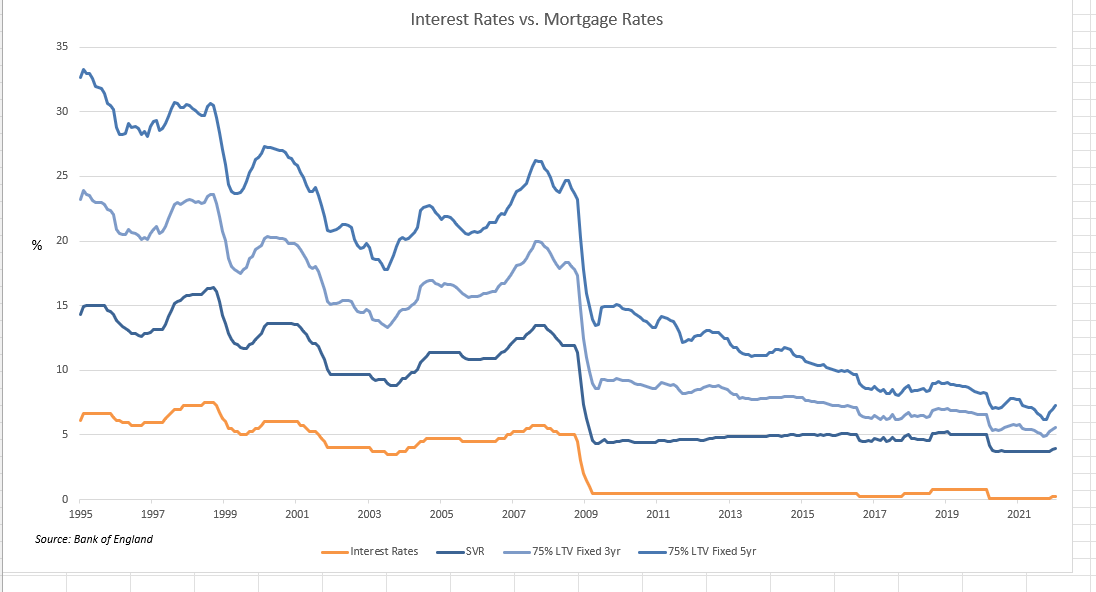

Addressing the first part to that question, if we were to assume that mortgage rates moved in line with the BBR (see below), then on a mortgage of £250,000, there would be an increase in monthly repayments of £54 as a result of the recent rate rise. If mortgage rates rose by a further 1.5%, as one could interpret from the current forward rate curve, monthly repayments on that same mortgage would rise by £210.

This could squeeze some homeowners and first-time buyers, especially when we consider the pressure that inflation – which is currently running at 5.5% in the UK – is putting on real incomes.

However, when considered in a historical context, interest rates do appear to be relatively low. For example, based on average lending rates, average incomes and house prices, borrowers are spending approximately 25% of their monthly income on mortgage repayments. If the BoE rate moved to 1% and this was mirrored in mortgage rates, that proportion would rise to approximately 28%. This compares to borrowers spending an average 42% of their income on mortgage repayments back in 2007.

It is also worth reminding ourselves that post-crisis regulation has meant that aspiring homeowners need to demonstrate that they can still service their mortgage even if the interest rate was stressed at 6% or 7%, which is significantly above the level the markets currently expect them to reach.

For these reasons, we feel that current expectations regarding rate rises, should they materialise, would prove to be on average more uncomfortable than unmanageable for borrowers. However, that’s not to say we are blind to the potential for interest rates to move higher, if inflation remains stubbornly high, and the impact this may have on residential prices.

Other Factors at Play

As alluded to earlier, we feel that borrowing costs and real wage growth will be the most significant factors influencing the demand for UK housing in the coming years, but supply side factors cannot be ignored.

Current estimates put the requirement for new housing in England alone at 340,000 a year, whereas delivered homes in 2020/21 and 2019/20 were 216,000 and 243,000 respectively.

This deficit has been a long term problem for the UK and the issue of undersupply is likely to persist unless the government can reform the planning system, provide further support for SME housebuilders and unlock large infrastructure projects, which is something that successive governments have failed to do. Until supply begins to meet the demand for housing, it will forever be a force providing upward support on the price of housing in the UK.

Outlook

The factors outlined above will continue to play a key role in determining the outlook for the UK residential market.

Our in-house view is that the steep rise in house prices we have seen since the start of the pandemic is not sustainable, and that growth will be more tempered as we move through 2022 and beyond, with forecast annual growth of around 2% through to 2024.

This is a view broadly in line with many of the established agents and institutions within the market – Office for Budget Responsibility (1.8% p.a.), Halifax mortgage provider (1% p.a.), Hamptons (3% p.a.), Savills (3% p.a).

That said, we are aware that uncertainty in the world is currently running high, particularly around inflation and interest rates, and that forecasts can quickly become outdated. This has been most recently evidenced by the ongoing conflict in Ukraine, with the impact being greatest on the lives of those involved, but also on global financial and economic markets. We are therefore focused on ensuring the performance of the fund can weather periods of increased volatility in the residential market.

With an average loan to value of 67%, and a weighted time-to-loan maturity of 6 months, the existing loan book offers a significant amount of downside protection. We also lend against the current market value of residential properties, meaning we are not reliant on house price growth to sustain performance. This approach is evidenced by the fund’s track record of stable performance despite movements in house prices.

However, going forward we are taking further steps to mitigate risk. These include:

- Increasing the granularity of the loan portfolio

- Reduced appetite for larger development loans

- Lowering the target weighted average loan to value

- Pricing larger and longer term loans on a variable rate to benefit from increasing interest rates

- Reviewing the headline rates of shorter term loans on an ongoing basis

Through this action, we believe that the fund will not only be well protected, but will be well positioned to take advantage of a changing interest rate environment.

Capital at risk – The value of investments (and income) may fall as well as rise and you may get back less than invested. Past performance is not a reliable indicator of future results. Learn more about our approach to managing risk.

Income and capital repayments are not guaranteed. Investors cannot liquidate investments, but the underlying borrowers may repay early, late or not at all. Your capital is at risk. Past performance is not a reliable indicator of future results.

The information we provide can help you make your own informed decisions, but it is not investment advice or a personal recommendation. You should seek independent financial advice if you are not sure a product or investment is right for you, or you do not fully understand the risks.

Issued by LendInvest Funds Management Limited (the Investment Advisor) on behalf of the LendInvest S.C.A SICAV-SIF S.A. – The LendInvest Real Estate Opportunity Fund which is authorised by the Commission de Surveillance du Secteur Financier.